Petroleum Liquid Feedstock Market Trends, Share and Industry Analysis, 2034

A raw material utilized in the manufacturing process to generate energy is referred to as feedstock. The petroleum liquid feedstock is a mixture of several different kinds of hydrocarbons, all of which are highly flammable and very volatile in their natural state.

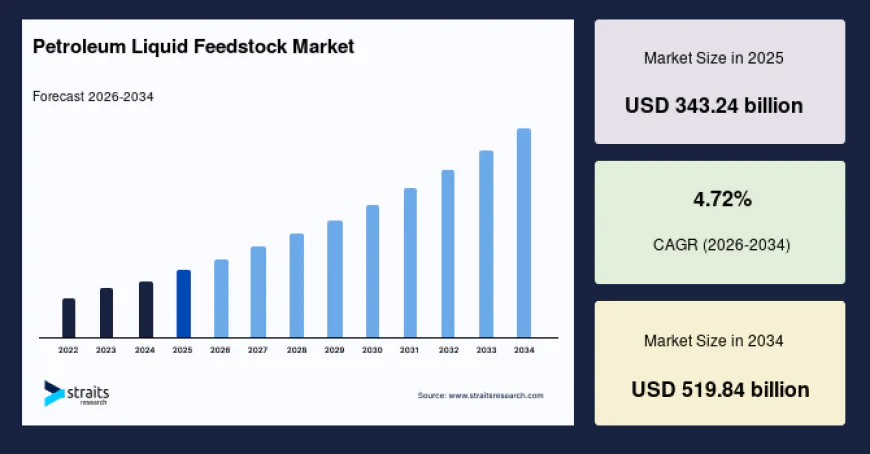

Market Overview

The global Petroleum Liquid Feedstock Market is experiencing significant growth due to increasing demand for petrochemicals, expanding refining capacities, and rising consumption of petroleum-derived products across various industries. Petroleum liquid feedstocks serve as essential raw materials in the production of chemicals, fuels, plastics, synthetic rubber, solvents, and numerous industrial products.

The growing industrialization in emerging economies, coupled with rising demand for energy and petrochemical products, is driving the market's expansion. Additionally, increasing investments in refinery modernization and petrochemical integration projects are supporting the adoption of advanced feedstock solutions. As global demand for downstream petroleum products continues to increase, the petroleum liquid feedstock market is expected to witness sustained growth throughout the forecast period.

The global petroleum liquid feedstock market was valued at USD 318.74 billion in 2024 and is projected to grow from USD 331.92 billion in 2025 to reach USD 462.58 billion by 2033, exhibiting a CAGR of 4.24% during the forecast period (2025–2033).

For detailed insights into market trends, competitive landscape, growth opportunities, regional analysis, and future forecasts, readers can explore the comprehensive report:

https://straitsresearch.com/report/petroleum-liquid-feedstock-market

Market Dynamics

Rising Demand from the Petrochemical Industry

One of the primary drivers of the petroleum liquid feedstock market is the growing demand from the petrochemical sector. Feedstocks such as naphtha, gas oil, and other petroleum liquids are extensively used to manufacture plastics, synthetic fibers, fertilizers, and industrial chemicals.

The rapid growth of industries such as packaging, automotive, construction, and consumer goods is increasing demand for petrochemical products, thereby driving feedstock consumption globally.

Expansion of Refining and Petrochemical Capacities

Governments and private companies are investing heavily in refinery expansion and petrochemical integration projects to meet rising energy and industrial demands. These investments are increasing the consumption of petroleum liquid feedstocks and supporting long-term market growth.

Modern refining technologies are also enabling more efficient feedstock utilization and enhanced production capabilities.

Growing Industrialization in Emerging Economies

Rapid industrial development across Asia-Pacific, the Middle East, and Latin America is contributing significantly to market expansion. The increasing need for fuels, chemicals, and industrial materials is creating substantial demand for petroleum-derived feedstocks.

Developing nations continue to invest in manufacturing and infrastructure projects, further supporting market growth.

Increasing Energy Consumption

Rising global energy demand, driven by population growth and economic development, is contributing to higher petroleum processing activities. Petroleum liquid feedstocks remain critical inputs for fuel production and various industrial applications.

Growing transportation, aviation, and manufacturing activities are expected to sustain demand during the forecast period.

Market Restraints

Volatility in Crude Oil Prices

Fluctuating crude oil prices remain a major challenge for the petroleum liquid feedstock market. Price instability can affect production costs, profit margins, and investment decisions across the value chain.

Environmental Regulations and Sustainability Concerns

Increasing environmental regulations aimed at reducing greenhouse gas emissions and promoting sustainable alternatives may limit long-term growth opportunities for petroleum-based products.

Governments worldwide are implementing stricter environmental standards that could impact refining operations and feedstock utilization.

Transition Toward Renewable Energy

The growing adoption of renewable energy sources and alternative raw materials presents a challenge for traditional petroleum feedstock markets. The transition toward cleaner energy systems may influence future demand patterns.

Market Opportunities

Growth of Petrochemical Manufacturing

The continued expansion of petrochemical production facilities presents significant opportunities for feedstock suppliers. Rising demand for polymers, synthetic materials, and specialty chemicals is expected to drive feedstock consumption.

Refinery Modernization Projects

Investments in advanced refining technologies are creating opportunities for improved feedstock efficiency and production optimization. Modern facilities can maximize output while reducing operational costs and environmental impact.

Emerging Markets Expansion

Developing economies continue to offer substantial growth potential due to increasing industrialization, urbanization, and infrastructure development activities. These regions are expected to remain key demand centers for petroleum liquid feedstocks.

Market Segmentation

By Feedstock Type

The market is segmented into:

-

Naphtha

-

Gas Oil

-

Kerosene

-

Liquefied Petroleum Gas (LPG)

-

Others

Naphtha accounts for a significant market share due to its extensive use in petrochemical manufacturing and chemical production processes.

By Application

The market includes:

-

Petrochemicals

-

Fuel Production

-

Industrial Chemicals

-

Plastics Manufacturing

-

Synthetic Materials

-

Others

Petrochemicals represent the dominant application segment owing to increasing demand for polymers, plastics, and industrial chemicals worldwide.

By End User

The market is categorized into:

-

Refineries

-

Petrochemical Companies

-

Chemical Manufacturers

-

Industrial Processing Facilities

-

Others

Petrochemical companies account for a substantial market share due to their extensive reliance on petroleum-based feedstocks for manufacturing operations.

Regional Analysis

Asia-Pacific

Asia-Pacific dominates the global petroleum liquid feedstock market due to rapid industrialization, strong petrochemical production capacities, and increasing energy consumption. Countries such as China, India, Japan, and South Korea are major contributors to regional demand.

The region continues to witness significant investments in refining and petrochemical infrastructure, supporting long-term market growth.

North America

North America represents a major market driven by advanced refining capabilities, strong petrochemical industries, and increasing investments in energy infrastructure.

The presence of major oil and gas companies further supports regional market expansion.

Europe

Europe maintains a significant market share supported by established refining industries and growing demand for specialty chemicals and industrial products.

The region is also focusing on improving refinery efficiency and sustainability initiatives.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth due to abundant crude oil reserves, expanding refining capacities, and increasing investments in downstream petroleum industries.

Countries in the Gulf region continue to strengthen their positions as major petrochemical production hubs.

Latin America

Latin America is witnessing gradual market growth supported by industrial development, refinery upgrades, and increasing demand for petroleum-derived products.

Emerging Market Trends

Several trends are shaping the future of the petroleum liquid feedstock market:

-

Expansion of integrated refinery and petrochemical complexes.

-

Increasing investments in advanced refining technologies.

-

Growing demand for petrochemical derivatives.

-

Rising focus on operational efficiency and feedstock optimization.

-

Development of cleaner refining processes.

-

Increasing adoption of digital technologies in refinery operations.

-

Strategic investments in downstream chemical manufacturing.

Competitive Landscape

The petroleum liquid feedstock market is highly competitive, with major energy and petrochemical companies focusing on production expansion, technological innovation, and strategic partnerships.

Market participants are investing in refining efficiency improvements, capacity expansion projects, and integrated petrochemical operations to strengthen their competitive positions.

Key Players

-

Saudi Aramco

-

Exxon Mobil Corporation

-

Shell plc

-

Chevron Corporation

-

BP plc

-

TotalEnergies SE

-

Reliance Industries Limited

-

Sinopec Group

-

PetroChina Company Limited

-

Kuwait Petroleum Corporation

These companies continue to expand their global operations and invest in advanced refining and petrochemical technologies to meet growing market demand.

Frequently Asked Questions

What is petroleum liquid feedstock?

Petroleum liquid feedstock refers to liquid hydrocarbon materials derived from crude oil that are used as raw materials in refining, petrochemical production, fuel manufacturing, and chemical processing industries.

What factors are driving market growth?

Major growth drivers include rising petrochemical demand, refinery expansion projects, increasing industrialization, and growing global energy consumption.

Which feedstock type dominates the market?

Naphtha holds a significant market share due to its extensive use in petrochemical and chemical manufacturing applications.

Which region leads the global market?

Asia-Pacific currently dominates the market owing to strong industrial growth, expanding petrochemical production, and increasing energy demand.

What opportunities exist in the market?

Key opportunities include refinery modernization, petrochemical capacity expansion, technological advancements, and growth in emerging economies.

Conclusion

The global petroleum liquid feedstock market is expected to witness steady growth through 2033, driven by expanding petrochemical industries, increasing energy demand, and ongoing investments in refining infrastructure. Despite challenges related to environmental regulations and energy transition initiatives, the market continues to benefit from strong industrial demand and growing downstream applications. As refining and petrochemical sectors evolve, petroleum liquid feedstocks will remain critical components of global industrial and energy value chains.