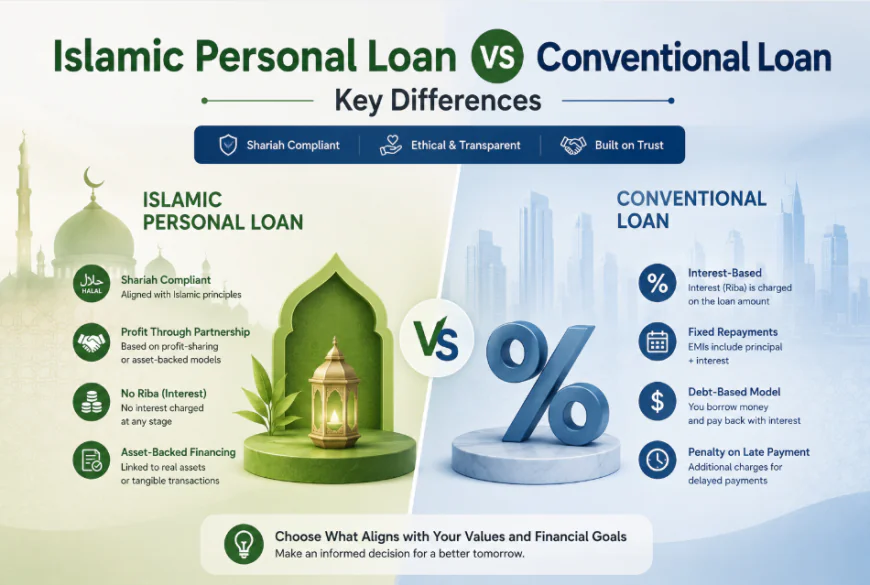

Islamic Personal Loan vs Conventional Loan: Key Differences

7. Ethical Investment Standards Islamic Personal Loan Islamic banks avoid financing industries considered non-compliant under Sharia law, such as: Gambling Alcohol Tobacco Unethical businesses Conventional Loan Conventional banks may finance a broader range of industries without religious restrictions.

amandamichael

amandamichael

Financial support has become an important part of modern life, especially for individuals looking to manage personal expenses, education costs, home renovations, travel plans, or emergencies. In the UAE, borrowers usually choose between two major financing options an Islamic personal loan and a conventional loan.

Both options provide financial assistance, but they operate differently in terms of structure, profit calculation, and financial principles. Understanding these differences is essential before applying for any loan in Dubai or across the UAE.

This blog explains the major differences between Islamic and conventional personal loans, helping you choose the right financing solution based on your financial goals and preferences.

What Is an Islamic Personal Loan?

An Islamic personal loan is a Sharia-compliant financing solution designed according to Islamic banking principles. Unlike traditional loans, Islamic financing does not involve interest (Riba), which is prohibited under Islamic law.

Instead of charging interest, Islamic banks use approved financial structures such as:

- Murabaha

- Tawarruq

- Ijara

The bank purchases goods or assets on behalf of the customer and sells them at a pre-agreed profit margin.

This system ensures transparency, ethical financing, and compliance with Islamic principles.

What Is a Conventional Loan?

A conventional loan is the traditional borrowing method offered by most banks and financial institutions. In this system, the bank lends money directly to the borrower and charges interest on the borrowed amount.

The borrower repays:

- Principal amount

- Interest charges

- Additional fees if applicable

Conventional loans are widely used for personal financing, business expansion, home purchases, and other financial needs.

Key Differences Between Islamic Personal Loan and Conventional Loan

1. Interest vs Profit Structure

The biggest difference between both financing options is how banks earn revenue.

Islamic Personal Loan

Islamic banks do not charge interest. Instead, they apply a fixed profit margin agreed upon before the financing begins.

This makes the financing process more transparent and predictable.

Conventional Loan

Conventional banks charge interest based on the loan amount and repayment period. Interest rates may be fixed or variable depending on the bank.

2. Compliance with Islamic Principles

Islamic Personal Loan

An Islamic personal loan follows Sharia law and ethical banking standards. It avoids:

- Interest-based transactions

- Unethical investments

- Unclear contract terms

This makes Islamic financing highly preferred among customers seeking religiously compliant financial solutions.

Conventional Loan

Conventional loans are not based on Islamic principles and operate under traditional banking systems that involve interest charges.

3. Loan Structure

Islamic Financing Structure

Islamic banks use asset-backed financing methods. Common structures include:

Murabaha

The bank purchases an asset and sells it to the customer with a profit margin.

Tawarruq

The bank buys commodities and sells them to the customer, allowing the customer to receive cash financing.

This structure ensures transactions are tied to actual assets or trade activities.

Conventional Loan Structure

The bank directly lends money to the borrower, who repays it with interest over time.

4. Transparency in Payments

Islamic Personal Loan

Islamic financing usually offers fixed repayment schedules with clearly defined profit amounts.

Customers know:

- Total repayment amount

- Monthly installment value

- Financing duration

This reduces uncertainty and financial confusion.

Conventional Loan

Interest rates in conventional loans can sometimes change depending on market conditions, especially with variable-rate loans.

This may affect monthly payments over time.

5. Late Payment Charges

Islamic Personal Loan

Islamic banks generally avoid profiting from late payment penalties. Some banks may impose charges, but these amounts are often donated to charity instead of becoming bank income.

Conventional Loan

Conventional banks usually apply additional interest or penalty fees for delayed payments.

This can increase the borrower’s overall financial burden.

6. Risk Sharing Principles

Islamic Personal Loan

Islamic banking promotes shared responsibility between the bank and customer. Transactions are based on ethical partnerships and trade-based activities.

Conventional Loan

In conventional banking, the borrower carries most of the financial risk and remains responsible for interest payments regardless of financial circumstances.

7. Ethical Investment Standards

Islamic Personal Loan

Islamic banks avoid financing industries considered non-compliant under Sharia law, such as:

- Gambling

- Alcohol

- Tobacco

- Unethical businesses

Conventional Loan

Conventional banks may finance a broader range of industries without religious restrictions.

Why Many UAE Residents Prefer Islamic Personal Loans

The demand for Islamic personal loan solutions has grown significantly in the UAE due to several advantages.

Ethical Banking

Many customers prefer ethical and transparent financial practices.

Predictable Repayments

Fixed profit structures help borrowers manage budgets more effectively.

Religious Compliance

Islamic financing aligns with Islamic financial principles, making it a preferred choice for many UAE residents.

Competitive Financing Options

Many Islamic banks now offer competitive profit rates and flexible repayment plans similar to conventional banks.

Advantages of Conventional Loans

Although Islamic financing is growing rapidly, conventional loans still remain popular due to several reasons.

Wider Product Availability

Conventional banks often provide a broader variety of loan products.

Flexible Loan Structures

Borrowers may find different repayment and refinancing options.

Faster Processing

Some conventional banks offer quick approvals for eligible applicants.

For many residents seeking a fast loan in Dubai, conventional financing remains a practical option.

How to Choose Between Islamic and Conventional Loans

Choosing the right financing option depends on your:

- Financial goals

- Religious preferences

- Repayment ability

- Banking requirements

Here are some important factors to compare:

Profit or Interest Rate

Always compare the total repayment amount.

Loan Tenure

Choose a repayment period suitable for your monthly income.

Processing Fees

Review hidden charges and administrative costs.

Early Settlement Policies

Check if there are fees for paying the financing early.

Flexibility

Look for repayment flexibility and customer support services.

Eligibility for Personal Loans in UAE

Whether applying for an Islamic or conventional loan, banks usually require:

- Valid Emirates ID

- UAE residency visa

- Minimum salary requirement

- Salary transfer to the bank

- Good credit history

Eligibility conditions may vary depending on the bank and financing type.

Digital Banking and Online Loan Applications

Today, applying for a loan in Dubai has become easier through digital banking platforms.

Most banks now allow customers to:

- Apply online

- Upload documents digitally

- Track application status

- Receive approvals faster

This digital transformation has improved customer convenience and reduced paperwork.

Future of Islamic Financing in UAE

The UAE continues to strengthen its position as a global Islamic finance hub. Islamic banking is expected to grow further due to:

- Increasing customer awareness

- Demand for ethical financing

- Government support for Islamic finance

- Digital banking innovations

As more customers seek transparent and ethical financial services, Islamic personal financing will likely continue expanding across the region.

Conclusion

Both Islamic and conventional loans offer valuable financial support, but they differ significantly in structure, principles, and repayment methods. An Islamic personal loan focuses on ethical, interest-free financing based on Sharia principles, while conventional loans rely on traditional interest-based systems.

Before choosing any loan in Dubai, borrowers should carefully compare profit rates, repayment terms, flexibility, and overall financial goals. Understanding the key differences can help you make a smarter and more informed financial decision.

FAQs

1. What is an Islamic personal loan?

An Islamic personal loan is a Sharia-compliant financing solution that avoids interest and follows Islamic banking principles.

2. How is an Islamic personal loan different from a conventional loan?

Islamic financing uses profit-based structures instead of charging interest, while conventional loans rely on interest payments.

3. Is an Islamic personal loan available in Dubai?

Yes, many UAE banks and Islamic financial institutions offer Islamic personal loan solutions in Dubai.

4. Are Islamic personal loans interest-free?

Islamic loans do not charge traditional interest but apply a pre-agreed profit margin under Sharia-compliant structures.

5. Can expatriates apply for a loan in Dubai?

Yes, expatriates can apply for both Islamic and conventional loans if they meet eligibility requirements.

6. Which is better: Islamic or conventional loan?

The better option depends on your financial goals, repayment ability, and preference for Sharia-compliant banking.

7. Can I apply for an Islamic personal loan online?

Yes, many UAE banks now offer online application services for Islamic personal financing.