Organ Transplant Diagnostics Market Size, Share and Forecast 2026–2034

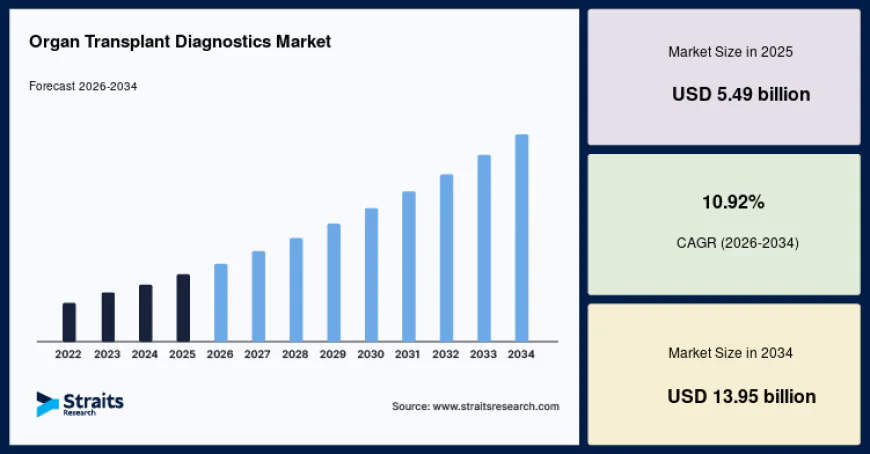

The global organ transplant diagnostics market size was valued at USD 5.49 billion in 2025 and is projected to grow from USD 6.09 billion in 2026 to USD 13.95 billion by 2034, registering a CAGR of 10.92% during the forecast period (2026–2034).

The global organ transplant diagnostics market is witnessing robust growth due to the increasing number of organ transplant procedures, rising prevalence of chronic diseases leading to organ failure, and continuous advancements in molecular diagnostic technologies. The global organ transplant diagnostics market size was valued at USD 5.49 billion in 2025 and is projected to grow from USD 6.09 billion in 2026 to USD 13.95 billion by 2034, registering a CAGR of 10.92% during the forecast period (2026–2034).

Organ transplant diagnostics play a critical role in evaluating donor-recipient compatibility, monitoring transplant recipients, and detecting organ rejection at an early stage. These diagnostic solutions include human leukocyte antigen (HLA) typing, antibody screening, molecular assays, and transplant monitoring tests that improve transplant success rates and patient outcomes. Increasing healthcare investments, growing awareness regarding organ donation, and the adoption of precision medicine are further supporting market expansion worldwide.

Market Drivers

One of the primary factors driving the organ transplant diagnostics market is the increasing prevalence of chronic diseases such as kidney failure, liver cirrhosis, heart disease, and lung disorders. The growing number of patients requiring organ transplantation has significantly increased the demand for accurate diagnostic testing before and after transplant procedures. Advanced diagnostics help improve donor-recipient matching and reduce the risk of transplant rejection.

Another significant growth driver is the rapid advancement of molecular diagnostic technologies. Innovations in next-generation sequencing (NGS), polymerase chain reaction (PCR), and high-resolution HLA typing have enhanced the accuracy and speed of transplant compatibility testing. These technologies enable clinicians to make informed treatment decisions while improving long-term transplant outcomes.

The increasing adoption of personalized medicine is also contributing to market growth. Healthcare providers are utilizing advanced diagnostic tools to monitor immune responses, detect donor-specific antibodies, and identify early signs of graft rejection, enabling timely clinical intervention and improved patient management.

Furthermore, rising government initiatives promoting organ donation, expanding transplant programs, and increasing investments in healthcare infrastructure are creating new growth opportunities. Growing collaborations between diagnostic companies, research institutions, and transplant centers are accelerating the development of innovative transplant diagnostic solutions.

Market Challenges

Despite favorable growth prospects, the organ transplant diagnostics market faces several challenges.

One of the major restraints is the high cost associated with advanced molecular diagnostic tests and specialized laboratory equipment. These costs may limit accessibility in developing countries with constrained healthcare budgets.

Another challenge is the global shortage of donor organs, which limits the number of transplant procedures performed despite increasing patient demand. This imbalance affects the overall growth potential of transplant-related diagnostic services.

Additionally, stringent regulatory requirements governing diagnostic products, laboratory accreditation, and clinical validation may increase development costs and delay product commercialization.

Market Segmentation

By Product

- Reagents and Consumables

- Instruments

- Software and Services

The reagents and consumables segment accounts for the largest market share due to their continuous use in HLA typing, antibody screening, crossmatching, and transplant monitoring procedures performed in diagnostic laboratories and transplant centers.

By Technology

- Molecular Assays

- Non-Molecular Assays

The molecular assays segment dominates the market owing to the increasing adoption of PCR, next-generation sequencing (NGS), and other advanced molecular techniques that provide highly accurate donor-recipient compatibility assessment and post-transplant monitoring.

By Transplant Type

- Kidney Transplant

- Liver Transplant

- Heart Transplant

- Lung Transplant

- Pancreas Transplant

- Others

The kidney transplant segment holds the largest market share due to the high global prevalence of chronic kidney disease and the increasing number of kidney transplant procedures performed each year.

Regional Insights

North America

North America dominates the global organ transplant diagnostics market due to advanced healthcare infrastructure, a high volume of organ transplant procedures, increasing adoption of molecular diagnostic technologies, and the presence of leading biotechnology and diagnostic companies. The United States continues to drive regional market growth through strong research investments and well-established transplant programs.

Europe

Europe represents a significant market supported by increasing organ donation awareness, favorable healthcare policies, expanding transplant registries, and continuous advancements in transplant diagnostics. Strong collaborations between healthcare providers and research institutions continue to strengthen regional growth.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period owing to improving healthcare infrastructure, rising incidence of chronic diseases, increasing healthcare expenditure, growing awareness regarding organ donation, and expanding transplant programs across China, India, Japan, South Korea, and Southeast Asian countries.

Latin America, Middle East, and Africa

These regions are emerging markets driven by improving access to transplant healthcare services, expanding diagnostic laboratory networks, increasing government support for organ transplantation, and rising investments in healthcare infrastructure.

Key Players Analysis

The organ transplant diagnostics market is highly competitive, with leading companies focusing on advanced molecular diagnostics, HLA typing technologies, transplant monitoring solutions, and strategic collaborations with healthcare institutions. Continuous investments in research and development are enabling manufacturers to introduce highly accurate and efficient diagnostic solutions that improve transplant success rates and patient outcomes.

Major companies operating in the market include:

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd.

- Bio-Rad Laboratories, Inc.

- Illumina, Inc.

- QIAGEN N.V.

- Abbott Laboratories

- CareDx, Inc.

- Hologic, Inc.

- Immucor, Inc.

- Omixon Biocomputing Ltd.

These companies continue expanding their transplant diagnostic portfolios, investing in next-generation molecular testing technologies, and strengthening global partnerships to meet the growing demand for precision transplant diagnostics.

For Detailed Insights, Visit:

https://straitsresearch.com/report/organ-transplant-diagnostics-market

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)