Intraosseous Devices Market Growth Analysis by Product, Application and Regional Outlook

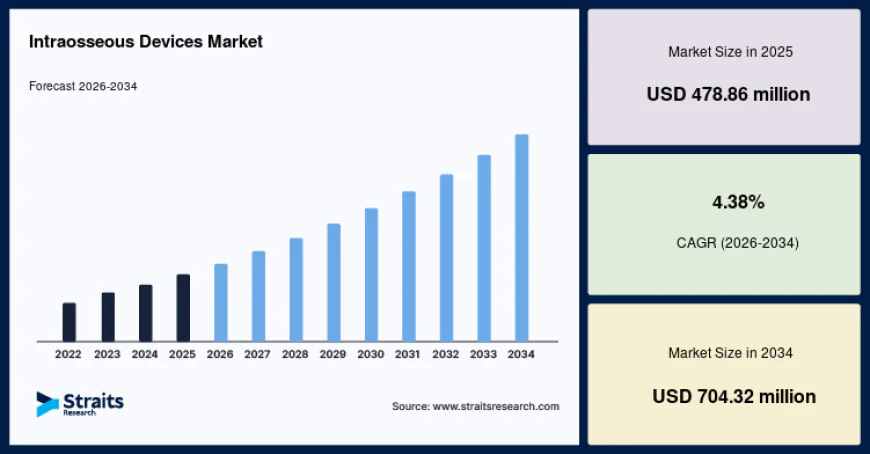

The global intraosseous devices market size was valued at USD 478.86 million in 2025 and is projected to grow from USD 499.84 million in 2026 to USD 704.32 million by 2034, registering a CAGR of 4.38% during the forecast period (2026–2034).

The global intraosseous devices market is witnessing steady growth due to the increasing demand for rapid vascular access during medical emergencies, rising incidence of trauma cases, and growing adoption of advanced emergency care technologies. The global intraosseous devices market size was valued at USD 478.86 million in 2025 and is projected to grow from USD 499.84 million in 2026 to USD 704.32 million by 2034, registering a CAGR of 4.38% during the forecast period (2026–2034).

Intraosseous devices are specialized medical instruments used to establish vascular access through the bone marrow when conventional intravenous (IV) access is difficult or impossible. These devices are widely used in emergency medicine, trauma care, critical care, military healthcare, and pediatric settings to administer fluids, blood products, and medications quickly. Growing awareness among healthcare professionals regarding the advantages of intraosseous access, coupled with advancements in device technology, is expected to support market growth during the forecast period.

Market Drivers

One of the primary factors driving the intraosseous devices market is the increasing incidence of medical emergencies and trauma cases worldwide. Road accidents, cardiac arrests, severe burns, shock, and natural disasters often require immediate vascular access for life-saving treatment. Intraosseous devices provide a rapid and reliable alternative when traditional intravenous access cannot be established quickly.

Another significant growth driver is the growing adoption of intraosseous access in emergency and critical care settings. Hospitals, emergency medical services (EMS), military medical units, and ambulance services are increasingly incorporating intraosseous devices into their emergency response protocols due to their speed, reliability, and high success rates.

Technological advancements in intraosseous devices are also contributing to market growth. Manufacturers are introducing battery-powered insertion systems, semi-automatic devices, and ergonomic needle designs that improve insertion accuracy, reduce procedure time, and enhance patient safety. These innovations are increasing clinician confidence and encouraging wider adoption across healthcare facilities.

Furthermore, the expansion of healthcare infrastructure, increasing emergency preparedness initiatives, and rising investments in advanced medical technologies are creating new opportunities for market participants. Government efforts to strengthen emergency response systems are further supporting demand for intraosseous access devices.

Market Challenges

Despite favorable growth prospects, the intraosseous devices market faces several challenges.

One of the major restraints is the relatively high cost of advanced intraosseous insertion systems, which may limit adoption among smaller healthcare facilities and institutions in developing countries.

Another challenge is the limited availability of trained healthcare professionals capable of performing intraosseous procedures safely and effectively. Proper training is essential to minimize complications and ensure successful device placement.

Additionally, the potential risk of complications such as infection, bone fractures, compartment syndrome, and incorrect needle placement may discourage adoption in certain clinical settings.

Market Segmentation

By Product

- Manual Intraosseous Devices

- Battery-Powered Intraosseous Devices

- Impact-Driven Intraosseous Devices

The battery-powered intraosseous devices segment accounts for the largest market share owing to their rapid insertion capabilities, ease of use, improved procedural accuracy, and widespread adoption in emergency and trauma care settings.

By Application

- Emergency Medicine

- Trauma Care

- Cardiac Arrest

- Pediatrics

- Others

The emergency medicine segment dominates the market due to the increasing use of intraosseous access during life-threatening emergencies where immediate vascular access is essential for administering medications and fluids.

By End User

- Hospitals

- Emergency Medical Services (EMS)

- Ambulatory Surgical Centers

- Military Medical Facilities

- Others

The hospitals segment holds the largest market share owing to the high volume of emergency procedures, availability of advanced critical care facilities, and increasing adoption of modern vascular access technologies.

Regional Insights

North America

North America dominates the global intraosseous devices market due to its advanced healthcare infrastructure, high adoption of emergency medical technologies, strong presence of leading medical device manufacturers, and well-established emergency medical services. The United States remains the largest contributor to regional market growth through continuous investments in trauma and critical care.

Europe

Europe represents a significant market driven by increasing healthcare expenditure, expanding emergency medical services, rising incidence of trauma cases, and growing adoption of advanced vascular access technologies. Government support for emergency healthcare infrastructure continues to strengthen regional demand.

Asia-Pacific

Asia-Pacific is expected to witness the fastest growth during the forecast period owing to improving healthcare infrastructure, rising healthcare investments, increasing awareness of emergency care technologies, and growing demand for advanced medical devices across China, India, Japan, South Korea, and Southeast Asian countries.

Latin America, Middle East, and Africa

These regions are emerging markets supported by expanding emergency healthcare services, increasing investments in hospital infrastructure, improving access to advanced medical technologies, and growing awareness regarding rapid vascular access procedures.

Key Players Analysis

The intraosseous devices market is highly competitive, with leading manufacturers focusing on product innovation, portable insertion systems, ergonomic device design, and strategic collaborations with healthcare providers. Continuous investments in research and development are enabling companies to introduce safer, faster, and more efficient intraosseous access solutions.

Major companies operating in the market include:

- Teleflex Incorporated

- Becton, Dickinson and Company

- PerSys Medical

- Cook Medical

- Pyng Medical Corporation

- Cardinal Health, Inc.

- SAM Medical

- Aero Healthcare

- Biopsybell S.r.l.

- Zhejiang Kindly Medical Devices Co., Ltd.

These companies continue expanding their product portfolios, investing in advanced intraosseous technologies, and strengthening their global distribution networks to meet the growing demand for emergency vascular access devices.

For Detailed Insights, Visit:

https://straitsresearch.com/report/intraosseous-devices-market

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.), +44 203 695 0070 (U.K.)