EV Semiconductors Market Industry Trends, Share & Forecast (2026–2034)

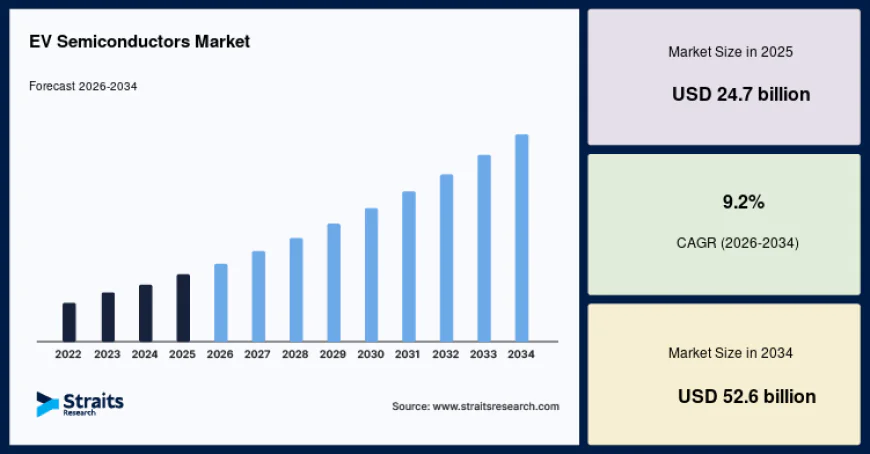

The global EV semiconductors market size is valued at USD 24.7 billion in 2025 and is estimated to reach USD 52.6 billion by 2034, growing at a CAGR of 9.2% during the forecast period.

EV Semiconductors Market

The EV Semiconductors Market is experiencing robust growth as the global automotive industry accelerates the transition toward electric mobility. The global EV semiconductors market size is valued at USD 24.7 billion in 2025 and is estimated to reach USD 52.6 billion by 2034, growing at a CAGR of 9.2% during the forecast period (2026–2034). Rising electric vehicle (EV) production, increasing government incentives for zero-emission transportation, and continuous advancements in semiconductor technologies are fueling market expansion across developed and emerging economies.

As electric vehicles become more sophisticated, demand for high-performance semiconductor components such as power devices, microcontrollers, sensors, and integrated circuits continues to rise. These components play a crucial role in battery management systems, powertrain control, charging infrastructure, autonomous driving technologies, and vehicle connectivity. With automotive manufacturers investing heavily in next-generation EV platforms, the EV Semiconductors Market is expected to witness sustained growth throughout the forecast period.

For detailed market insights, growth forecasts, and competitive analysis, visit: https://straitsresearch.com/report/ev-semiconductors-market

Market Drivers

Rising Global Adoption of Electric Vehicles

One of the primary growth drivers for the EV Semiconductors Market is the rapid increase in electric vehicle adoption worldwide. Governments across North America, Europe, and Asia-Pacific are implementing stringent emission regulations, tax incentives, and subsidies to encourage EV adoption. Automotive manufacturers are expanding their electric vehicle portfolios, increasing the demand for advanced semiconductor components that enhance vehicle efficiency, performance, and safety.

Growing Demand for Advanced Power Electronics

Modern electric vehicles rely on sophisticated power electronics to optimize battery performance and energy efficiency. Wide-bandgap semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) are gaining popularity due to their superior thermal performance, faster switching capabilities, and improved energy efficiency. These advanced semiconductor technologies enable longer driving ranges, faster charging, and improved overall vehicle reliability.

Expansion of Autonomous and Connected Vehicle Technologies

Electric vehicles are increasingly equipped with advanced driver assistance systems (ADAS), artificial intelligence, vehicle-to-everything (V2X) communication, and autonomous driving capabilities. These technologies require high-performance processors, sensors, memory chips, and communication modules. As automotive manufacturers continue integrating smart technologies into electric vehicles, semiconductor demand is expected to increase significantly over the coming years.

Market Challenges

Semiconductor Supply Chain Constraints

The global semiconductor industry has experienced supply chain disruptions due to geopolitical tensions, raw material shortages, and manufacturing capacity limitations. These challenges have affected automotive production schedules and delayed EV deliveries. Ensuring a resilient semiconductor supply chain remains a key priority for manufacturers and governments seeking to meet growing electric vehicle demand.

High Manufacturing Costs

Advanced automotive semiconductors require sophisticated fabrication processes, specialized materials, and significant research and development investments. The high production cost of next-generation semiconductor technologies can increase overall electric vehicle manufacturing expenses, particularly during the early stages of technology adoption. Cost optimization and production scalability remain important challenges for industry participants.

Market Segmentation

By Component

The EV Semiconductors Market is segmented into:

- Power Semiconductors

- Microcontrollers (MCUs)

- Integrated Circuits (ICs)

- Sensors

- Memory Devices

- Communication Chips

- Others

Power semiconductors account for the largest market share due to their critical role in battery management systems, inverters, and electric powertrains. Meanwhile, sensors and communication chips are expected to experience the fastest growth as connected and autonomous vehicle technologies continue to evolve.

By Vehicle Type

The market includes:

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

Battery Electric Vehicles dominate the market because they require a greater number of semiconductor components for propulsion, battery management, charging systems, and onboard electronics. The rapid global shift toward fully electric transportation continues to strengthen demand within this segment.

By Application

Major application areas include:

- Battery Management Systems

- Powertrain

- Infotainment Systems

- Safety and Security Systems

- Charging Infrastructure

- Telematics and Connectivity

Battery management systems represent the leading application segment, ensuring battery safety, efficiency, thermal management, and charging optimization. Charging infrastructure is expected to register rapid growth as governments and private organizations continue expanding public EV charging networks worldwide.

Regional Insights

North America

North America remains a leading market for EV semiconductors, supported by increasing electric vehicle production, substantial investments in semiconductor manufacturing, and favorable government policies promoting clean transportation. The United States is witnessing strong demand for advanced automotive electronics driven by growing EV adoption, technological innovation, and expansion of domestic semiconductor production capabilities.

Europe

Europe holds a significant share of the EV Semiconductors Market due to ambitious carbon reduction targets, strict vehicle emission regulations, and widespread adoption of electric mobility. Germany, France, the United Kingdom, and the Nordic countries continue investing in EV manufacturing, battery production, and semiconductor research to strengthen regional competitiveness and accelerate sustainable transportation initiatives.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth during the forecast period. China, Japan, South Korea, and India have become global leaders in electric vehicle production and semiconductor manufacturing. Government incentives, expanding charging infrastructure, strong consumer demand, and continuous investments in automotive innovation are driving rapid market expansion across the region. China remains the largest producer and consumer of electric vehicles, creating significant opportunities for semiconductor suppliers.

Latin America, Middle East & Africa

The EV Semiconductors Market in Latin America and the Middle East & Africa is gradually expanding as governments encourage electric mobility and invest in sustainable transportation infrastructure. Countries such as Brazil, the United Arab Emirates, Saudi Arabia, and South Africa are implementing policies to support EV adoption and develop charging networks. Although market penetration remains relatively low, increasing environmental awareness and infrastructure investments are expected to support long-term regional growth.

Key Players Analysis

The EV Semiconductors Market is highly competitive, with leading semiconductor manufacturers focusing on technological innovation, strategic partnerships, capacity expansion, and research into next-generation power semiconductor materials. Companies are investing in silicon carbide and gallium nitride technologies, automotive-grade integrated circuits, artificial intelligence processors, and advanced power management solutions to strengthen their competitive positions and support the growing electric vehicle industry.

Major companies operating in the market include:

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Toshiba Electronic Devices & Storage Corporation

- Wolfspeed Inc.

- Qualcomm Incorporated

- NVIDIA Corporation

- Analog Devices Inc.

- Microchip Technology Inc.

- Semiconductor Components Industries LLC

- Mitsubishi Electric Corporation

Conclusion

The EV Semiconductors Market is positioned for substantial growth as the automotive industry accelerates the adoption of electric mobility, intelligent transportation systems, and connected vehicle technologies. Rising demand for electric vehicles, advancements in power electronics, increasing investments in charging infrastructure, and innovations in semiconductor materials are creating significant opportunities for manufacturers worldwide. Although supply chain challenges and high production costs remain important considerations, ongoing investments in semiconductor manufacturing and research are expected to strengthen market resilience. With the market projected to reach USD 52.6 billion by 2034 at a CAGR of 9.2% during 2026–2034, the EV Semiconductors Market is expected to remain a critical enabler of the future electric mobility ecosystem.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)