Warts Treatment Market: Comprehensive Analysis and Growth Outlook

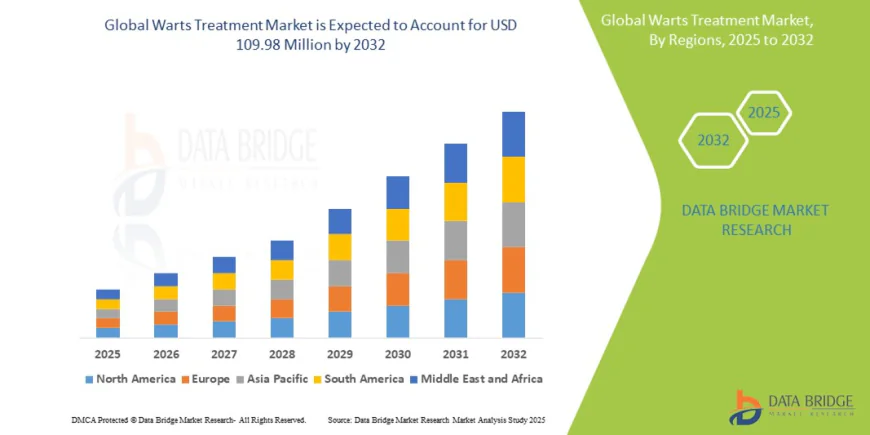

The global warts treatment market size was valued at USD 82.88 million in 2024 and is expected to reach USD 109.98 million by 2032, at a CAGR of 3.60% during the forecast period

vikasdada

vikasdada

The global warts treatment market represents a significant segment within the dermatology and healthcare industry, addressing one of the most common skin conditions affecting millions of people worldwide. Warts, caused primarily by human papillomavirus (HPV) infections, manifest as benign skin growths that can appear on various parts of the body, including hands, feet, face, and genital areas. The market encompasses a diverse range of treatment options, from traditional topical medications to advanced laser therapies and immunotherapy approaches.

The healthcare industry has witnessed substantial growth in the warts treatment sector, driven by increasing awareness about skin health, rising prevalence of HPV infections, and continuous technological advancements in treatment methodologies. Healthcare providers and pharmaceutical companies have invested heavily in developing innovative solutions that offer better efficacy, reduced treatment duration, and improved patient comfort. This market serves both prescription and over-the-counter segments, catering to different severity levels and patient preferences.

The warts treatment market has experienced consistent expansion due to several factors, including growing healthcare expenditure, increasing disposable income in emerging economies, and enhanced accessibility to dermatological services. The market also benefits from the rising trend of aesthetic consciousness among consumers, who seek effective solutions for skin imperfections. Healthcare professionals have recognized the importance of providing comprehensive treatment options that address both medical and cosmetic concerns associated with wart infections.

Modern treatment approaches have evolved significantly from traditional methods, incorporating cutting-edge technologies and evidence-based practices. The integration of telemedicine and digital health platforms has further expanded market reach, enabling remote consultations and treatment monitoring. This digital transformation has been particularly beneficial during the COVID-19 pandemic, as patients sought alternative ways to access healthcare services while maintaining social distancing protocols.

The Evolution of Warts Treatment

The treatment landscape for warts has undergone remarkable transformation over the past several decades, evolving from crude removal methods to sophisticated, targeted therapies. Historical approaches to wart treatment included harsh chemical applications, surgical excision, and folk remedies with varying degrees of success and significant side effects. The understanding of wart pathophysiology was limited, leading to treatments that focused primarily on physical removal rather than addressing the underlying viral cause.

Early medical interventions relied heavily on destructive methods such as electrocautery, surgical excision, and aggressive chemical peeling agents. These approaches, while sometimes effective, often resulted in scarring, pain, and high recurrence rates. The lack of understanding about HPV's role in wart formation meant that treatments were largely symptomatic rather than targeting the root cause of the infection.

The introduction of cryotherapy using liquid nitrogen marked a significant advancement in wart treatment during the mid-20th century. This method offered a less invasive alternative to surgical removal while providing reasonable efficacy rates. Cryotherapy became widely adopted in dermatology practices due to its relative simplicity and effectiveness, particularly for common warts on hands and feet. The technique involves freezing the wart tissue, causing cellular destruction and stimulating an immune response against the virus.

Topical treatments experienced substantial development with the introduction of salicylic acid formulations, imiquimod cream, and other keratolytic agents. These medications offered patients the convenience of home-based treatment while providing gradual but effective wart removal. The development of various concentrations and delivery systems allowed healthcare providers to customize treatment approaches based on wart location, size, and patient tolerance.

The advent of laser technology revolutionized wart treatment by providing precise, controlled tissue destruction with minimal damage to surrounding healthy skin. Carbon dioxide lasers, pulsed dye lasers, and neodymium-doped yttrium aluminum garnet lasers each offered unique advantages for different types of warts. Laser treatments demonstrated superior cosmetic outcomes compared to traditional methods, making them particularly attractive for facial and genital warts where scarring was a significant concern.

Immunotherapy approaches emerged as a groundbreaking development in wart treatment, focusing on enhancing the body's natural immune response to clear HPV infections. Contact sensitizers, intralesional immunotherapy, and systemic immune modulators provided new options for recalcitrant warts that failed to respond to conventional treatments. These approaches recognized that successful wart clearance required not just tissue destruction but also immune system activation to prevent recurrence.

Recent advances have introduced combination therapies that leverage multiple treatment modalities simultaneously or sequentially. These approaches have shown improved clearance rates and reduced recurrence compared to single-agent treatments. The development of personalized medicine concepts in dermatology has led to treatment protocols tailored to individual patient characteristics, wart subtypes, and immune status.

Current Market Trends

The warts treatment market is experiencing several significant trends that are reshaping the industry landscape and influencing treatment approaches worldwide. The shift toward minimally invasive procedures has gained substantial momentum, with patients increasingly preferring treatments that offer effective results with minimal discomfort and downtime. This trend has driven innovation in topical formulations, laser technologies, and immunotherapy options that provide superior patient experiences compared to traditional methods.

Digital health integration has become a prominent trend, with telemedicine platforms enabling remote consultations and treatment monitoring. Healthcare providers are leveraging mobile applications and digital imaging technologies to track treatment progress and adjust protocols without requiring frequent in-person visits. This approach has proven particularly valuable for managing chronic or recurrent wart cases that require long-term monitoring and care.

The over-the-counter segment has experienced remarkable growth, with consumers seeking convenient, cost-effective solutions for wart management. Pharmaceutical companies have responded by developing sophisticated home-use products that incorporate professional-grade active ingredients in user-friendly formulations. These products often include instructional materials, application tools, and monitoring guidelines to ensure safe and effective use.

Combination therapy protocols have gained widespread acceptance among healthcare providers, with evidence supporting enhanced efficacy when multiple treatment modalities are used together. These approaches often combine topical medications with physical destruction methods or immunotherapy agents to maximize clearance rates and minimize recurrence. The development of standardized combination protocols has improved treatment outcomes and reduced the trial-and-error approach previously common in wart management.

Preventive approaches have garnered increased attention, with healthcare providers emphasizing patient education about HPV transmission and prevention strategies. This trend has led to the development of protective products, hygiene protocols, and lifestyle modifications that can reduce wart acquisition risk. The integration of prevention strategies with treatment protocols has shown promise in reducing recurrence rates and overall disease burden.

The aesthetic dermatology influence has significantly impacted treatment selection, with patients prioritizing cosmetic outcomes alongside therapeutic efficacy. This trend has driven demand for treatments that provide excellent clearance rates while minimizing scarring, hyperpigmentation, and other aesthetic complications. Healthcare providers are increasingly considering cosmetic factors when selecting treatment approaches, particularly for visible body areas.

Pediatric treatment considerations have become more prominent, with specialized protocols developed specifically for children who represent a significant portion of wart patients. These approaches emphasize pain reduction, anxiety management, and age-appropriate treatment modalities. The development of child-friendly formulations and treatment techniques has improved compliance and outcomes in pediatric populations.

Research and development investments have intensified, with pharmaceutical companies and biotechnology firms exploring novel therapeutic targets and delivery mechanisms. This trend has led to pipeline products that promise improved efficacy, reduced treatment duration, and better patient tolerability. The focus on understanding HPV biology and host immune responses has opened new avenues for therapeutic intervention.

Challenges Facing the Market

The warts treatment market confronts several significant challenges that impact both healthcare providers and patients seeking effective therapeutic solutions. Treatment resistance remains one of the most persistent challenges, with certain wart types and locations demonstrating poor response to conventional therapies. Recalcitrant warts, particularly those in immunocompromised patients or specific anatomical locations, often require multiple treatment attempts and extended therapy duration, leading to patient frustration and increased healthcare costs.

Recurrence rates present another substantial challenge, with studies indicating that warts can return in 20-30% of cases even after apparently successful treatment. This phenomenon occurs due to incomplete viral clearance, reinfection, or immune system inadequacy in maintaining long-term viral suppression. The unpredictability of recurrence makes treatment planning difficult and affects patient confidence in therapeutic interventions.

Pain and discomfort associated with many treatment modalities continue to be significant barriers to patient compliance and treatment completion. Procedures such as cryotherapy, laser treatment, and surgical excision can cause considerable pain, particularly in sensitive areas or when treating large warts. The development of effective pain management strategies remains an ongoing challenge for healthcare providers.

Treatment cost considerations create barriers to access, particularly for advanced therapies such as laser treatments and immunotherapy options. Many insurance plans provide limited coverage for wart treatments, considering them cosmetic rather than medical necessities. This coverage limitation disproportionately affects patients with extensive or recurrent warts who require multiple treatment sessions or expensive therapeutic modalities.

Scarring and cosmetic complications represent serious concerns, especially for warts on visible body areas such as face and hands. Traditional destructive methods can leave permanent marks that may be more cosmetically objectionable than the original warts. Balancing treatment efficacy with aesthetic outcomes requires careful consideration and skilled technique from healthcare providers.

Patient compliance challenges arise from treatment duration requirements, application complexity, and side effect tolerance. Many effective treatments require weeks or months of consistent application, and patient adherence often decreases over time. The development of user-friendly formulations and treatment protocols that maximize compliance while maintaining efficacy remains an ongoing challenge.

Diagnostic accuracy issues can complicate treatment selection, as various skin conditions can mimic warts, leading to inappropriate treatment choices. Misdiagnosis may result in treatment failure, unnecessary procedures, and delayed appropriate therapy. Healthcare provider education about differential diagnosis and the judicious use of confirmatory testing such as dermoscopy or biopsy is essential.

Regulatory challenges affect product development and market entry, particularly for novel therapeutic approaches. The approval process for new wart treatments can be lengthy and expensive, requiring extensive clinical trials to demonstrate safety and efficacy. Regulatory requirements vary between countries, creating additional complexity for companies seeking global market presence.

Healthcare provider training and expertise limitations impact treatment outcomes, as optimal results often depend on proper technique and treatment selection. The wide range of available therapies and their specific indications require ongoing education and skill development. Ensuring consistent quality of care across different healthcare settings remains challenging.

Market Scope and Applications

The warts treatment market encompasses a comprehensive range of therapeutic approaches, delivery systems, and target applications that address diverse patient needs and clinical scenarios. The scope extends across multiple healthcare settings, from primary care physician offices and dermatology clinics to specialized aesthetic centers and home-based treatment environments. This broad scope reflects the varied nature of wart presentations and patient preferences for treatment locations and methodologies.

Treatment modalities within the market scope include topical medications such as salicylic acid, imiquimod, tretinoin, and various keratolytic agents that offer convenient home-based therapy options. These formulations are available in multiple delivery systems including gels, solutions, patches, and foam preparations designed to optimize drug penetration and patient compliance. The topical segment represents the largest market share due to its accessibility, cost-effectiveness, and ease of use.

Cryotherapy applications constitute a significant portion of the market scope, utilizing liquid nitrogen or other cryogenic agents to destroy wart tissue through controlled freezing. This treatment modality is widely available in healthcare facilities and has established efficacy for most wart types. Recent innovations have introduced home-use cryotherapy devices that provide controlled cold application for patient self-treatment under medical supervision.

Laser therapy applications span multiple technologies including carbon dioxide lasers, pulsed dye lasers, and erbium lasers, each offering specific advantages for different wart characteristics and anatomical locations. The laser segment continues to expand with technological improvements that enhance precision, reduce pain, and improve cosmetic outcomes. These treatments are primarily available in specialized dermatology and aesthetic medicine facilities.

Immunotherapy approaches within the market scope include contact sensitizers such as diphencyprone, intralesional immunotherapy using candida antigen or interferon, and systemic immune modulators. These treatments target the underlying immune response to HPV infection and are particularly valuable for recalcitrant cases that have failed conventional therapies. The immunotherapy segment represents a growing portion of the market as understanding of wart immunology advances.

Surgical and procedural interventions encompass electrocautery, curettage, excision, and minimally invasive techniques that provide immediate wart removal. These approaches are typically reserved for large, resistant, or rapidly growing warts that require prompt intervention. The procedural segment benefits from technological advances that reduce invasiveness and improve healing outcomes.

The market scope extends to various wart types and anatomical locations, including common warts on hands and fingers, plantar warts on feet, flat warts on face and body, and genital warts requiring specialized treatment approaches. Each application area has specific therapeutic considerations regarding efficacy, safety, and cosmetic outcomes that influence treatment selection and market dynamics.

Pediatric applications represent a substantial market segment, with age-appropriate formulations and treatment protocols designed specifically for children. These products emphasize safety, ease of application, and pain reduction while maintaining therapeutic efficacy. The pediatric market continues to grow as awareness of childhood wart prevalence increases among parents and healthcare providers.

Home-use treatment products have expanded significantly within the market scope, offering consumers convenient alternatives to clinic-based treatments. These products include over-the-counter topical medications, cryotherapy devices, and combination treatment kits that provide comprehensive wart management solutions. The home-use segment benefits from consumer preference for privacy, convenience, and cost savings.

Prevention and maintenance products are emerging within the market scope, including protective barriers, antiviral formulations, and immune-supporting supplements designed to reduce wart acquisition risk and prevent recurrence. This preventive approach represents a growing market opportunity as healthcare shifts toward proactive rather than reactive treatment strategies.

Market Size and Growth Projections

The global warts treatment market has demonstrated substantial growth momentum over recent years, with market valuation reaching approximately $3.2 billion in 2024. Industry analysts project continued expansion at a compound annual growth rate of 6.8% through 2030, driven by increasing prevalence of HPV infections, growing awareness of treatment options, and technological advancements in therapeutic approaches. This growth trajectory positions the warts treatment market as one of the more dynamic segments within the broader dermatology therapeutics industry.

Regional market distribution reveals significant variations in market size and growth patterns across different geographical areas. North America currently represents the largest market share at approximately 40% of global valuation, driven by high healthcare expenditure, advanced medical infrastructure, and strong awareness of dermatological treatments. The United States dominates the North American market with robust demand for both prescription and over-the-counter treatment options.

The European market accounts for roughly 30% of global market share, with Germany, France, and the United Kingdom leading regional growth. European markets benefit from comprehensive healthcare coverage, increasing aesthetic consciousness, and well-established dermatology practices. The European Medicines Agency's supportive regulatory environment has facilitated the introduction of innovative treatment options across member countries.

Asia-Pacific represents the fastest-growing regional market, with projected compound annual growth rates exceeding 8.5% through 2030. This growth is fueled by large population bases, increasing healthcare expenditure, rising disposable incomes, and expanding access to dermatological services. China and India represent particularly significant growth opportunities due to their massive populations and improving healthcare infrastructure.

The over-the-counter segment dominates market revenue, accounting for approximately 65% of total market value. This segment's growth is driven by consumer preference for convenient, cost-effective solutions and the availability of sophisticated home-use products. Major pharmaceutical companies have invested heavily in developing advanced OTC formulations that rival prescription alternatives in efficacy while maintaining safety for unsupervised use.

Prescription medications represent about 25% of market share, with topical immunomodulators and prescription-strength keratolytic agents leading this segment. The prescription market benefits from healthcare provider preference for proven efficacy and the availability of specialized formulations for complex or resistant cases. Insurance coverage for prescription treatments varies significantly between markets, influencing segment growth rates.

Professional treatment procedures, including laser therapy, cryotherapy, and surgical interventions, account for approximately 10% of market revenue but command higher profit margins. This segment is expected to experience robust growth as technological advances reduce treatment costs and improve accessibility. The expanding aesthetic dermatology market is driving demand for advanced procedural treatments that offer superior cosmetic outcomes.

Market size analysis by wart type reveals that common warts represent the largest treatment volume, followed by plantar warts and flat warts. Genital warts represent a smaller but high-value segment due to the complexity of treatment and the need for specialized healthcare provider intervention. The distribution reflects the relative prevalence of different wart types in the general population.

The pediatric segment represents approximately 35% of total market volume, reflecting the high prevalence of warts in children and adolescents. This segment is characterized by specific product requirements including child-friendly formulations, safety considerations, and parent-administered treatments. Market growth in pediatric applications is supported by increasing awareness among parents and healthcare providers about the importance of early treatment intervention.

Emerging markets in Latin America, Middle East, and Africa collectively represent about 15% of current market share but demonstrate high growth potential. These markets benefit from improving healthcare infrastructure, increasing awareness of dermatological conditions, and expanding access to treatment options. Economic development in these regions is expected to drive substantial market expansion over the forecast period.

The direct-to-consumer market segment has experienced exceptional growth, particularly through e-commerce channels and digital health platforms. Online sales of wart treatment products have increased significantly, driven by consumer preference for privacy, competitive pricing, and convenient delivery options. This segment is expected to continue robust growth as digital commerce becomes more prevalent in healthcare product distribution.

Factors Driving Market Growth

Multiple interconnected factors are propelling the expansion of the global warts treatment market, creating a favorable environment for sustained growth across various market segments and geographical regions. The increasing prevalence of human papillomavirus infections worldwide serves as a primary growth driver, with epidemiological studies indicating rising incidence rates across different age groups and populations. This trend is particularly pronounced in developing countries where improving diagnostic capabilities are revealing previously underestimated disease burden.

Growing awareness and education about wart treatment options have significantly contributed to market expansion, as patients become more informed about available therapeutic approaches and their respective benefits. Healthcare campaigns, digital health information platforms, and increased media coverage of dermatological conditions have empowered consumers to seek appropriate treatment rather than ignoring or attempting ineffective home remedies. This awareness transformation has particularly impacted the over-the-counter segment, as consumers become more confident in self-treatment approaches.

Technological advancements in treatment modalities continue to drive market growth by offering improved efficacy, reduced side effects, and enhanced patient experience. Innovations in laser technology, topical drug delivery systems, and immunotherapy approaches have expanded treatment options and improved outcomes for previously difficult-to-treat cases. These advances have also enabled the development of home-use devices and formulations that bring professional-grade treatments to consumer markets.

The expanding aesthetic consciousness among consumers has become a significant growth driver, as individuals increasingly seek treatment for cosmetic rather than purely medical reasons. Social media influence, professional appearance requirements, and general beauty trends have elevated the importance of clear, healthy-looking skin. This trend has particularly benefited treatments that offer superior cosmetic outcomes, driving demand for advanced laser therapies and minimally invasive procedures.

Demographic shifts, including aging populations in developed countries and expanding middle classes in emerging markets, have created favorable conditions for market growth. Older adults often have accumulated wart exposure over their lifetime and possess the financial resources to pursue effective treatment. Meanwhile, emerging market populations with increasing disposable income are gaining access to previously unavailable treatment options.

Healthcare infrastructure improvements in developing countries have expanded access to dermatological services and wart treatments, opening new markets for pharmaceutical companies and medical device manufacturers. The establishment of dermatology clinics, training of healthcare providers, and improvement of supply chains have made treatments available to previously underserved populations.

The integration of telemedicine and digital health platforms has revolutionized treatment accessibility, enabling remote consultations and monitoring that expand the effective reach of healthcare providers. This technological integration has been particularly valuable during the COVID-19 pandemic, maintaining treatment continuity while reducing infection risks. Digital platforms have also facilitated patient education and compliance monitoring, improving treatment outcomes.

Research and development investments have accelerated innovation in the warts treatment space, with pharmaceutical companies and biotechnology firms pursuing novel therapeutic targets and delivery mechanisms. Pipeline products promise improved efficacy, reduced treatment duration, and better patient tolerability, creating anticipation and investment interest that drives overall market growth.

Regulatory support and approval of new treatment options have facilitated market expansion by providing healthcare providers and patients with additional therapeutic choices. Regulatory agencies have streamlined approval processes for certain treatment categories, particularly those with established safety profiles, enabling faster market introduction of innovative products.

Insurance coverage improvements in many markets have reduced financial barriers to treatment, making advanced therapies more accessible to broader patient populations. While coverage remains variable, the trend toward recognizing wart treatment as medically necessary rather than purely cosmetic has improved reimbursement scenarios.

The prevention and wellness trend in healthcare has created opportunities for products and services that focus on reducing wart acquisition risk and preventing recurrence. This shift toward proactive healthcare has expanded the market beyond treatment to include preventive products and educational services.

Economic factors including rising healthcare expenditure, increasing disposable income, and growing health insurance penetration in emerging markets have created favorable conditions for market growth. These economic trends enable more patients to access treatment options and drive demand for premium therapeutic approaches.

The medical tourism industry has contributed to market growth by facilitating access to advanced treatments in countries with specialized expertise and cost advantages. Patients increasingly travel across borders to access cutting-edge wart treatments, creating international market opportunities for healthcare providers and treatment manufacturers.

Professional medical education and training improvements have enhanced healthcare provider capabilities in wart treatment, leading to better patient outcomes and increased confidence in recommending various therapeutic approaches. This educational advancement has particularly benefited complex treatment modalities that require specialized knowledge and skills.

The integration of artificial intelligence and machine learning in diagnostic and treatment selection processes has improved treatment success rates and reduced trial-and-error approaches. These technological advances have enhanced healthcare provider confidence and patient satisfaction, contributing to market growth through improved outcomes and word-of-mouth recommendations.

Other Trending Reports

https://www.databridgemarketresearch.com/reports/global-treatment-resistant-depression-market

https://www.databridgemarketresearch.com/reports/global-straw-market

https://www.databridgemarketresearch.com/reports/global-chromatography-columns-market

https://www.databridgemarketresearch.com/reports/global-bleached-eucalyptus-kraft-pulp-market

https://www.databridgemarketresearch.com/reports/global-smoke-detector-market

https://www.databridgemarketresearch.com/reports/global-magnetic-beads-market

https://www.databridgemarketresearch.com/reports/global-graph-database-market

https://www.databridgemarketresearch.com/reports/global-vented-caps-market