India Food Processing Market Valuation to Reach INR 65,835.0 Billion by 2034, at 7.72% CAGR

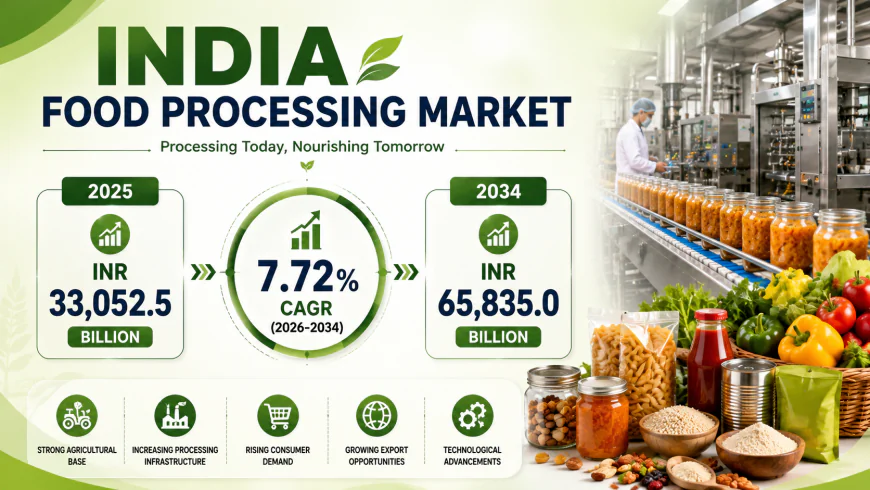

The food processing market in India reached INR 33,052.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach INR 65,835.0 Billion by 2034, exhibiting a growth rate (CAGR) of 7.72% during 2026-2034.

According to IMARC Group's report titled "India Food Processing Market Size, Share, Trends and Forecast by Sector, and Region, 2026-2034", the report offers a comprehensive analysis of the industry, including food processing market share in India, its growth, trends, and regional insights.

The food processing market in India reached INR 33,052.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach INR 65,835.0 Billion by 2034, exhibiting a growth rate (CAGR) of 7.72% during 2026-2034. India's large and diverse population, coupled with rising disposable incomes and changing lifestyles, is fueling the demand for processed and convenience foods, primarily driving market growth. This market is not speculative; it is being driven by increased urbanization, a shift towards hectic work schedules, the government's supportive policies and initiatives, significant advancements in technology, and escalating consumer awareness of food safety and quality standards.

Market Key Statistics:

- Current Market Size (2025): INR 33,052.5 Billion

- Projected Market Size (2034): INR 65,835.0 Billion

- CAGR: 7.72%

- Forecast Period: 2026-2034

- Packaged foods represent the largest sector segment, driven by rising health and wellness awareness, increasing urbanization, and growing demand for RTE meals and convenience items among time-constrained consumers.

- West India holds the largest regional market share, supported by its strong concentration of food processing infrastructure, established manufacturing hubs, and efficient trade networks.

- The Make in India campaign has been extended to the food processing sector, attracting domestic and foreign investments and enabling the government to set up dedicated food parks and processing units with infrastructure support and incentives.

- The implementation of GST has simplified the tax structure for food manufacturers, streamlining processes and enhancing the ease of doing business, presenting remunerative opportunities for market expansion.

India Food Processing Market Trends & Future Outlook

- Large and Diverse Population with Changing Lifestyles: India's population is one of the largest globally, with a diverse mix of consumers representing various cultural backgrounds and dietary preferences. Increasing urbanization and rising disposable incomes have led to changes in consumer preferences and eating habits, with more people moving to cities and leading hectic lifestyles creating a growing inclination towards processed and convenient foods. The rising trend of nuclear families and working professionals also contributes to the preference for RTE meals and packaged foods that require minimal preparation, strengthening market growth.

- Supportive Government Policies and Initiatives: The Government of India is actively promoting the food processing sector through various policies and initiatives. The Make in India campaign has been extended to the food processing sector, attracting domestic and foreign investments. The government has set up dedicated food parks and processing units, offering infrastructural support and incentives to encourage businesses in this sector, helping reduce logistics costs and improve supply chain efficiencies. The enactment of GST has further simplified the tax structure, streamlining processes for food manufacturers and enhancing the ease of doing business.

- Rising Demand for Ready-to-Eat and Convenience Food Products: The surge in preference for packaged and ready-to-eat meals is creating a strong favorable outlook for market expansion. Food processing enables the production of RTE meals, pre-cut fruits, vegetables, and other convenience items, catering to time-constrained consumers seeking quick and hassle-free meal solutions. Simultaneously, food processing extends the shelf life of packaged foods, reducing food wastage and ensuring a stable supply of products to meet the demands of modern-day consumers.

- Technological Advancements Improving Food Processing Efficiency: Significant advancements in technology and innovation are enabling efficient food processing methods that improve product quality and reduce post-harvest losses. Advanced technologies such as pasteurization, dehydration, and extrusion play vital roles in the systematic transformation of raw ingredients into edible and marketable food products, presenting remunerative growth opportunities for the market.

- Rising Health Consciousness Driving Nutritionally Enriched Products: The rise in awareness of health and wellness among consumers has resulted in increased demand for minimally processed and nutritionally enriched packaged foods. Food processing techniques allow manufacturers to incorporate functional ingredients, fortify products with essential nutrients, and reduce undesirable components, aligning with the health-conscious choices of an increasingly informed consumer base.

Why Invest in the India Food Processing Market - Key Growth Drivers

- Expanding Working Women Population Driving Convenience Food Demand: The expanding working women population, along with the increasing demand for processed foods such as ready-to-eat products and snacks that require limited time for cooking and meal preparation, is primarily driving the India food processing market and creating significant opportunities for manufacturers and investors across product categories.

- Government's Make in India and Food Park Initiatives Attracting Investment: Government initiatives including the Make in India campaign, establishment of dedicated food parks, and processing units are providing crucial infrastructure support and incentives that are attracting both domestic and foreign investments into the food processing sector, creating a conducive ecosystem for sustained market growth.

- Rising Urbanization and Nuclear Family Culture: Rapid urbanization and the increasing prevalence of nuclear families and working professionals are creating a sustained demand for packaged and convenience food products. This structural shift in household composition and lifestyle patterns is a fundamental long-term growth driver for the food processing industry across India.

- Technological Innovation Reducing Post-Harvest Losses: Advanced food processing methods and technologies are enabling manufacturers to significantly reduce post-harvest losses while improving product quality and shelf life. This reduction in wastage not only improves the economics of food production but also ensures more stable and reliable supply chains across the country.

- E-Commerce Expansion Accelerating Processed Food Distribution: The COVID-19 pandemic led to a changing consumer inclination from conventional brick-and-mortar distribution channels towards e-commerce platforms for the purchase of processed food in India. This shift toward digital channels has opened significant new distribution pathways for food processing companies, enabling broader geographic reach and direct-to-consumer capabilities.

Key Market Challenges

- Supply Chain Inefficiencies and Cold Chain Limitations: Inadequate cold chain infrastructure and supply chain inefficiencies continue to constrain the distribution of perishable processed food products, resulting in quality variability and post-harvest losses that limit market expansion, particularly in tier-II and tier-III cities and rural areas.

- Regulatory Compliance and Food Safety Standards: Escalating consumer awareness of food safety and quality standards is compelling manufacturers to maintain high production standards and comply with evolving regulations, creating additional compliance costs and operational complexity, particularly for small and medium-sized enterprises in the sector.

- Intense Market Competition Between MNCs and Local Players: The competitive landscape features intense rivalry between large multinational corporations, established domestic players, and cost-competitive local and regional food processing companies, creating persistent pricing pressure and requiring continuous investment in product innovation, distribution, and brand differentiation.

Market Segmentation Breakdown

- Dairy

- Fruits and Vegetables

- Meat and Poultry Processing

- Fisheries

- Packaged Foods

- Beverages

- Others

Packaged foods represent the largest segment

Breakup by Region:

- North India

- South India

- East India

- West India

West India holds the largest share of the market

Competitive Landscape - By IMARC GROUP

The competitive landscape of the food processing market in India is characterized by a diverse mix of players, ranging from large multinational corporations to small and medium-sized enterprises and local players. Key players deploy various strategies including product innovation and diversification, expansion of distribution networks, and effective marketing to enhance market penetration. Detailed profiles of all major companies have been provided in the full research report.

Latest Developments & Industry Moves

- The government's dedicated food parks and processing units under the Make in India initiative continue to attract investments from both domestic and international food processing companies, reducing logistics costs and improving supply chain efficiencies across the sector.

- The implementation of GST has simplified the tax structure for food manufacturers across India, streamlining compliance processes and enhancing the ease of doing business, enabling both large and small players to operate more efficiently.

- Advancements in food processing technologies including pasteurization, dehydration, and extrusion are enabling manufacturers to improve product quality, reduce post-harvest losses, and extend shelf life, presenting remunerative growth opportunities for the broader market.

Request Customized Data Tailored to Your Interest

Note: If you require any specific information not covered within this report's scope, we will provide it as part of the customization.

Frequently Asked Questions

Q1. What was the size of the India food processing market in 2025?

➤ The India food processing market was valued at INR 33,052.5 Billion in 2025, making it one of the largest and most strategically important food manufacturing sectors in Asia with significant growth potential across all processed food categories.

Q2. What is the expected growth rate of the India food processing market during 2026-2034?

➤ The market is expected to exhibit a CAGR of 7.72% during 2026-2034, reaching INR 65,835.0 Billion by 2034 — driven primarily by the expanding working women population, rising demand for RTE products, government initiatives, and technological advancements in food processing.

Q3. Which sector holds the largest market share?

➤ Packaged foods currently hold the majority of the total market share, driven by rising health and wellness awareness, increasing urbanization, busy consumer lifestyles, and growing demand for convenient, shelf-stable food products that require minimal preparation time.

Q4. What has been the impact of COVID-19 on the India food processing market?

➤ The sudden outbreak of the COVID-19 pandemic led to the changing consumer inclination from conventional brick-and-mortar distribution channels towards e-commerce platforms for the purchase of processed food in India, permanently accelerating digital distribution adoption across the sector.

Q5. What are the key regions in the India food processing market?

➤ On a regional level, the market has been classified into North India, South India, East India, and West India, where West India currently dominates the market due to its strong manufacturing infrastructure, established trade networks, and high urban consumer density.

Conclusion

India's food processing market growth trajectory to INR 65,835.0 Billion by 2034 is structurally anchored in one of the world's most consequential intersections of a large and growing population, rising disposable incomes, and rapidly evolving consumer lifestyles. The convergence of government-backed investment in food parks and processing units under Make in India, the accelerating shift toward packaged and ready-to-eat food formats among urban and working consumers, the expansion of e-commerce distribution enabling new market reach, and a 7.72% CAGR growth trajectory are converging to sustain a growth story that is both durable and accelerating through the forecast period.

Verified Data Source: IMARC Group

IMARC Group is a global management consulting firm that helps ambitious changemakers create a lasting impact. The company offers comprehensive market assessment, feasibility studies, incorporation support, regulatory assistance, branding and strategy services, and procurement research.