Global IoT in Construction Market Competitive Analysis and Forecast 2026–2034

Modern infrastructure projects are increasingly incorporating connected HVAC systems, intelligent lighting, smart security platforms, and energy management solutions.

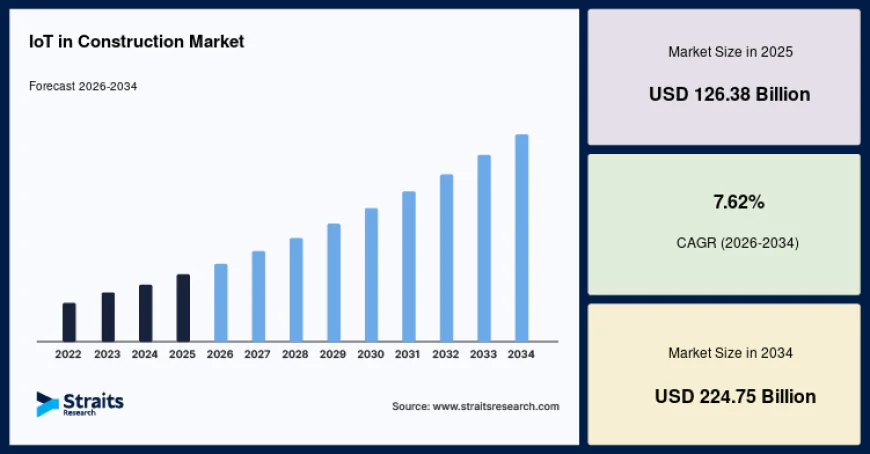

IoT in Construction Market

The global IoT in construction market is witnessing significant transformation as construction companies increasingly deploy connected technologies to improve productivity, enhance worker safety, and optimize project execution. The market was valued at USD 126.38 billion in 2025 and is projected to grow from USD 136.01 billion in 2026 to USD 224.75 billion by 2034, registering a compound annual growth rate (CAGR) of 7.62% during the forecast period from 2026 to 2034.

The construction industry is rapidly transitioning toward data-driven operations, supported by advancements in connected sensors, cloud platforms, wearable technologies, and real-time analytics. IoT-enabled systems are enabling construction firms to gain greater visibility into equipment performance, workforce safety, material utilization, and overall site operations. As infrastructure projects become larger and more complex, digital technologies are increasingly being integrated to improve decision-making, reduce project delays, and support sustainable construction practices.

Market Overview

The growing integration of connected technologies across construction sites is fundamentally changing how projects are planned, executed, and monitored. IoT solutions provide continuous streams of operational data, allowing project managers to monitor equipment, workforce activity, environmental conditions, and asset performance in real time. These capabilities are helping contractors reduce operational inefficiencies while improving safety and compliance outcomes.

The market's expansion is also being supported by the increasing adoption of smart city initiatives, modernization of public infrastructure, and greater emphasis on sustainability and carbon accountability. In parallel, advances in edge computing and industrial connectivity are enabling faster processing of site-level data, creating more responsive and automated construction environments.

Asia Pacific accounted for the largest market share of 28.33% in 2025, while North America is expected to emerge as the fastest-growing regional market throughout the forecast period, expanding at a CAGR of 13.11%.

Growth Drivers

One of the primary factors driving market growth is the increasing adoption of IoT-enabled wearable technologies for worker safety. Construction organizations are moving away from periodic manual supervision toward continuous digital monitoring systems that track fatigue, falls, vital signs, and hazardous exposure. Smart helmets, connected vests, and wearable sensors are enabling supervisors to identify risks proactively and respond more effectively to workplace incidents.

Industry studies indicate that wearable IoT technologies have contributed to approximately 40% reductions in workplace injuries across general industrial environments, while deployments in high-risk settings have demonstrated injury reductions ranging from 50% to 60%.

In addition, government regulations related to infrastructure modernization, environmental reporting, and carbon accountability are accelerating adoption. Public infrastructure projects increasingly require contractors to provide digital documentation on emissions, resource consumption, and project progress. As a result, connected sensors and automated reporting platforms are becoming essential tools for regulatory compliance and sustainability management.

Emerging Trends Reshaping the Industry

A notable trend influencing market development is the transition toward real-time IoT-based environmental monitoring across construction sites. Connected sensors are increasingly being used to monitor air quality, noise levels, weather conditions, and hazardous gases continuously rather than relying solely on manual inspections. This approach enhances worker safety, strengthens regulatory compliance, and supports sustainability objectives.

Another significant trend is the growing deployment of GPS and RFID-enabled equipment tracking systems. Construction firms are increasingly replacing conventional asset management methods with digital tracking platforms capable of monitoring machinery, tools, and materials in real time. These systems improve equipment utilization, reduce idle time, and enhance operational efficiency across large and geographically dispersed construction projects.

The integration of IoT technologies with building information modeling (BIM), automated machinery, and digital project management platforms is also gaining momentum, creating more connected and intelligent construction ecosystems.

Challenges Continue to Influence Adoption

Despite favorable growth prospects, several challenges continue to restrain widespread market adoption.

High implementation costs remain a major barrier, particularly for small and medium-sized contractors operating in cost-sensitive markets. The deployment of sensors, gateways, connectivity infrastructure, software platforms, and system integration services often requires substantial upfront investment. Ongoing maintenance, upgrades, and training expenses further increase total ownership costs.

Cybersecurity concerns also represent a significant challenge. As construction operations become increasingly connected, IoT devices and networks may become vulnerable to unauthorized access, data breaches, and cyberattacks. Security incidents affecting equipment monitoring systems or project management platforms could disrupt site operations, create safety risks, and delay project completion. Consequently, many construction firms continue to approach full-scale digital transformation cautiously.

Opportunities for Market Participants

The integration of smart building systems presents substantial opportunities for technology providers and construction firms alike. Modern infrastructure projects are increasingly incorporating connected HVAC systems, intelligent lighting, smart security platforms, and energy management solutions. These technologies enable continuous monitoring and optimization of building performance throughout the asset lifecycle.

Edge computing is creating additional growth opportunities by enabling faster data processing directly at construction sites. By reducing reliance on centralized cloud infrastructure, edge-enabled systems can support low-latency applications such as structural health monitoring, predictive maintenance, worker safety management, and autonomous equipment coordination. These capabilities are particularly valuable for large-scale projects operating in environments with limited network connectivity.

Regional Insights

Asia Pacific maintained its leadership position in the global IoT in construction market in 2025, supported by rapid urbanization, extensive infrastructure development, and accelerating smart city initiatives across major economies including China and India. Large-scale investments in transportation, residential, and public infrastructure projects continue to stimulate demand for connected construction technologies throughout the region.

China remains a major contributor to regional growth due to government initiatives promoting digital infrastructure, industrial IoT, and smart construction practices. Meanwhile, India's market expansion is being supported by substantial investments in highways, metro rail systems, airports, and urban development projects. Continued expansion of the country's infrastructure network is encouraging broader deployment of IoT-enabled monitoring and project management solutions.

North America is anticipated to record the fastest growth through 2034. The region's strong technology ecosystem, high investment capacity, and widespread adoption of advanced construction technologies are supporting rapid market expansion. In the United States, increasing use of connected sensors, drones, and automated monitoring systems is improving project visibility and operational efficiency across major infrastructure developments. Canada is also witnessing increased adoption as public infrastructure modernization and smart urban development projects gain momentum.

Segment Analysis

Based on application, asset monitoring emerged as the leading segment in 2025, accounting for 25.67% of total market revenue. The segment's dominance reflects growing demand for real-time tracking of construction equipment, tools, and materials to improve utilization and reduce operational inefficiencies.

Fleet management is expected to experience robust growth during the forecast period, registering a CAGR of 15.65%. Increasing demand for telematics solutions capable of monitoring vehicle movement, fuel consumption, equipment health, and driver behavior is supporting segment expansion.

By end user, the non-residential segment is projected to expand at a CAGR of 16.89% through 2034, driven by the complexity and scale of infrastructure, industrial, healthcare, and hospitality projects. Residential construction is also expected to record strong growth as developers increasingly deploy connected technologies to improve cost control, resource management, and project coordination.

By component, hardware accounted for the largest market share of 57.8% in 2025, reflecting strong demand for connected sensors, gateways, wearable devices, and edge computing infrastructure. The services segment is expected to witness significant growth as organizations increasingly require integration, maintenance, consulting, and support services to maximize the value of IoT deployments.

Competitive Landscape

The global IoT in construction market remains highly fragmented, characterized by the presence of multinational technology providers, construction equipment manufacturers, cloud service companies, and specialized IoT solution developers.

Leading participants are focused on strengthening integrated solution portfolios, enhancing interoperability, improving cybersecurity capabilities, and expanding partnerships across the construction ecosystem. Market competition increasingly centers on advanced analytics capabilities, end-to-end platform reliability, and scalable deployment models.

Key companies operating in the market include Trimble, Inc., Pillar Technologies Inc., Triax Technologies, Inc., Amazon Web Services, AOMS Technologies, Topcon Corporation, Hilti Corporation, Autodesk, Inc., Oracle Corporation, Hexagon AB, CalAmp Corporation, John Deere, SAP SE, Intel Corporation, and Qualcomm Technologies.

Recent industry developments highlight continued innovation in connected construction technologies. In October 2025, Trimble expanded integration between IoT-enabled jobsite data systems and its construction management platforms to enhance field connectivity and real-time asset tracking. During the same month, John Deere integrated Trimble Earthworks machine control technology into its SmartGrade platform, supporting greater interoperability across connected construction equipment ecosystems.

Click to Read the Complete Insights & Report https://straitsresearch.com/report/iot-in-construction-market

About Straits Research

Straits Research is a leading market research and intelligence organization providing actionable insights, customized research solutions, and comprehensive industry analysis across multiple sectors worldwide. The company delivers in-depth market reports covering emerging trends, competitive landscapes, growth opportunities, and strategic developments to help organizations make informed business decisions. Straits Research serves clients across industries including technology, healthcare, chemicals, energy, automotive, consumer goods, and advanced manufacturing through data-driven research methodologies and expert analysis.