Epoxy Resin Market: Transforming Industries Through Advanced Polymer Technology

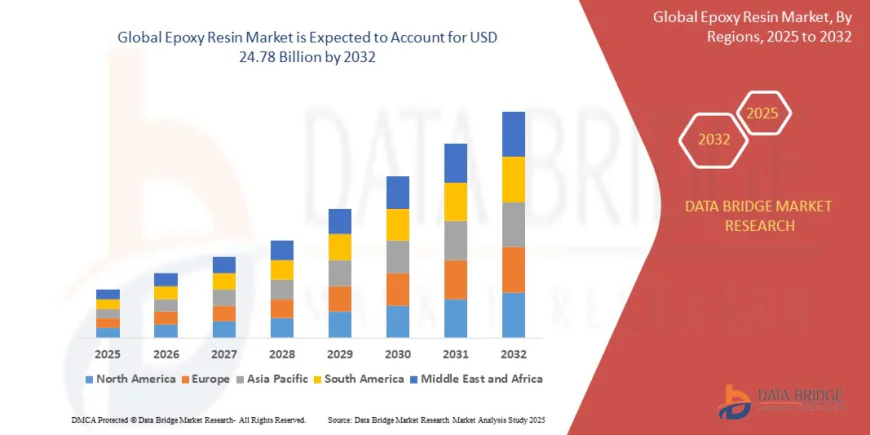

The global epoxy resin market size was valued at USD 14.84 billion in 2024 and is expected to reach USD 24.78 billion by 2032, at a CAGR of 6.62% during the forecast period

vikasdada

vikasdada

Introduction

Epoxy resins represent one of the most versatile and widely utilized classes of thermosetting polymers in modern industrial applications. These advanced materials combine exceptional mechanical properties, chemical resistance, and adhesive capabilities to create solutions that have become indispensable across numerous sectors. The unique molecular structure of epoxy resins, characterized by epoxide groups that undergo cross-linking reactions during curing, enables the formation of highly durable, three-dimensional polymer networks with outstanding performance characteristics.

The global epoxy resin market encompasses a diverse range of formulations including liquid resins, solid resins, and specialty grades designed for specific applications. These materials serve critical functions in construction, automotive manufacturing, electronics, aerospace, marine, and countless other industries where superior bonding strength, chemical resistance, and durability are essential requirements. The versatility of epoxy chemistry allows for precise tailoring of properties through molecular modification and the incorporation of various additives and reinforcements.

Modern epoxy resin systems offer remarkable design flexibility, enabling engineers and manufacturers to create solutions that meet increasingly demanding performance specifications. From structural adhesives capable of withstanding extreme environmental conditions to high-performance composites used in aerospace applications, epoxy resins continue pushing the boundaries of what is possible in material science. The ongoing development of bio-based epoxy resins and environmentally friendly formulations demonstrates the industry's commitment to sustainability while maintaining performance excellence.

The construction industry particularly benefits from epoxy resin technology, utilizing these materials for flooring systems, structural repairs, protective coatings, and adhesive applications that require long-term durability and reliability. Similarly, the electronics sector relies heavily on epoxy resins for encapsulation, printed circuit board manufacturing, and component protection in demanding operating environments.

The automotive industry has increasingly adopted epoxy-based solutions for lightweighting initiatives, corrosion protection, and structural bonding applications that contribute to improved fuel efficiency and performance. The aerospace sector continues expanding its use of epoxy matrix composites for critical structural components where weight reduction and strength are paramount considerations.

The Evolution of Epoxy Resin Technology

The development of epoxy resin technology began in the 1930s when Swiss chemist Pierre Castan and American chemist Sylvan Greenlee independently discovered methods for creating epoxy polymers through the reaction of epichlorohydrin with bisphenol A. These pioneering efforts laid the foundation for what would become one of the most important polymer technologies of the modern era.

During the 1940s and 1950s, commercial production of epoxy resins began in earnest as manufacturers recognized the exceptional properties these materials offered compared to existing alternatives. Early applications focused primarily on protective coatings and electrical insulation where the superior chemical resistance and mechanical properties of epoxy resins provided significant advantages over conventional materials.

The 1960s marked a period of rapid expansion as epoxy resin technology matured and new applications emerged across multiple industries. The aerospace industry began incorporating epoxy matrix composites into aircraft structures, recognizing the exceptional strength-to-weight ratios these materials could achieve. The construction industry simultaneously discovered the benefits of epoxy-based flooring systems and structural adhesives for demanding applications.

The 1970s and 1980s witnessed significant advances in epoxy chemistry with the development of specialized formulations designed for specific applications. Heat-resistant grades for automotive and aerospace use, rapid-curing systems for manufacturing efficiency, and environmentally resistant formulations for marine applications all emerged during this period. The electronics industry's growing sophistication drove development of ultra-pure epoxy resins for semiconductor encapsulation and printed circuit board manufacturing.

The 1990s brought revolutionary changes with the introduction of toughened epoxy systems that addressed the inherent brittleness of traditional formulations. These advanced materials incorporated elastomeric modifiers and thermoplastic additives to improve impact resistance and fracture toughness while maintaining the desirable properties of conventional epoxy resins.

The early 2000s saw increasing focus on environmental considerations as manufacturers developed low-volatile organic compound (VOC) formulations and water-based epoxy systems. These environmentally friendly alternatives addressed growing regulatory requirements while maintaining performance characteristics essential for critical applications.

Recent decades have witnessed remarkable innovation in epoxy resin technology with the development of bio-based feedstocks, nanocomposite formulations, and smart materials with self-healing capabilities. Advanced manufacturing techniques including resin transfer molding, vacuum-assisted resin transfer molding, and automated fiber placement have expanded the possibilities for epoxy-based composite manufacturing.

The emergence of additive manufacturing technologies has created new opportunities for epoxy resin applications in 3D printing and rapid prototyping. These applications demand specialized formulations with precise curing characteristics and dimensional stability.

Current Market Trends Shaping the Industry

The epoxy resin market is experiencing dynamic transformation driven by several converging trends that are reshaping application landscapes and creating new growth opportunities. Sustainability initiatives have become a dominant force, with manufacturers investing heavily in bio-based epoxy formulations derived from renewable feedstocks such as plant oils, lignin, and other natural materials.

The construction industry's evolution toward high-performance building materials has created substantial demand for advanced epoxy flooring systems, structural adhesives, and repair materials. Green building standards and energy efficiency requirements are driving adoption of epoxy-based solutions that contribute to improved building performance and longevity. The infrastructure modernization needs in both developed and emerging markets continue creating opportunities for specialized epoxy applications.

Automotive industry transformation toward electric vehicles and lightweighting strategies has significantly increased demand for epoxy-based composites and adhesives. Battery encapsulation systems require specialized epoxy formulations with exceptional thermal management properties and long-term reliability. Structural bonding applications that enable multi-material vehicle designs rely on advanced epoxy adhesives with superior bonding strength across dissimilar substrates.

The electronics industry's relentless pursuit of miniaturization and performance enhancement drives continuous innovation in epoxy encapsulation materials and circuit board applications. 5G technology deployment, artificial intelligence processors, and Internet of Things devices all require specialized epoxy formulations capable of protecting sensitive components while maintaining signal integrity and thermal management.

Renewable energy infrastructure development has opened significant new markets for epoxy resins in wind turbine blade manufacturing, solar panel encapsulation, and energy storage applications. The demanding operating environments and long service life requirements in these applications drive demand for highly durable epoxy formulations with exceptional weather resistance.

Advanced manufacturing technologies including automated composite production, resin infusion processes, and digital manufacturing techniques are reshaping how epoxy resins are processed and applied. These technologies enable more efficient production while maintaining quality and consistency standards essential for critical applications.

The aerospace and defense sectors continue expanding their use of epoxy matrix composites for next-generation aircraft and space systems. Advanced fighter aircraft, commercial aviation platforms, and space exploration vehicles all rely on sophisticated epoxy-based materials for structural components and specialized applications.

Marine industry growth in recreational boating, commercial shipping, and offshore energy applications creates steady demand for marine-grade epoxy systems with exceptional water resistance and durability. The development of larger, more sophisticated vessels drives requirements for advanced composite materials and protective coating systems.

Key Challenges Facing the Market

The epoxy resin market faces several significant challenges that influence development strategies and market dynamics across all application segments. Raw material price volatility represents one of the most persistent challenges as epoxy resin production relies heavily on petrochemical feedstocks whose prices fluctuate with global oil markets and supply chain disruptions.

Environmental regulations continue evolving across different regions, creating complexity for manufacturers who must navigate varying requirements for volatile organic compound emissions, hazardous air pollutants, and worker safety standards. The development of compliant formulations often requires substantial research investment and may involve performance trade-offs that affect market acceptance.

Competition from alternative materials presents ongoing challenges as other polymer technologies and adhesive systems continue improving their performance characteristics. Polyurethane systems, structural acrylics, and advanced thermoplastic materials all compete for market share in various applications, forcing epoxy resin manufacturers to continuously innovate and demonstrate superior value propositions.

Technical complexity in application development requires substantial investment in customer support and technical service capabilities. Each application often demands customized formulations and specialized processing techniques, creating challenges for both manufacturers and end users. The need for specialized equipment and trained personnel can limit adoption rates in some market segments.

Supply chain vulnerabilities have become more apparent as global disruptions affect availability of key raw materials and intermediate chemicals. The specialized nature of many epoxy resin ingredients creates dependencies on limited supplier bases, potentially impacting production consistency and cost stability.

Health and safety considerations require ongoing attention as epoxy resins and their curing agents can present occupational health challenges if not properly handled. Regulatory requirements for worker protection, product labeling, and safety documentation create compliance costs and complexity for manufacturers and users.

Processing challenges related to cure time, temperature sensitivity, and shelf life requirements can limit application possibilities and create logistics complications. Many epoxy systems require precise mixing ratios and controlled curing conditions, which can be difficult to achieve in certain application environments.

Market education remains necessary as many potential users are unfamiliar with the capabilities and proper application techniques for advanced epoxy systems. Demonstrating value propositions and return on investment requires significant technical support and educational efforts.

Quality control requirements in critical applications demand sophisticated testing and certification processes that can increase costs and time-to-market for new products. Aerospace, automotive, and electronics applications often require extensive qualification programs before new materials can be approved for use.

Market Scope and Application Segments

The epoxy resin market encompasses an extensive range of applications across diverse industries, each leveraging the unique properties of these versatile polymers for specific performance requirements. The construction and building sector represents the largest application segment, utilizing epoxy resins for flooring systems, structural adhesives, repair materials, and protective coatings that demand exceptional durability and chemical resistance.

Construction applications span from industrial flooring systems in manufacturing facilities and warehouses to decorative flooring in commercial and residential settings. Structural repair applications utilize epoxy resins for concrete crack injection, structural member reinforcement, and seismic retrofitting of existing buildings. The superior adhesion properties and chemical resistance of epoxy systems make them ideal for harsh industrial environments where conventional materials would fail.

The automotive industry has become increasingly important as manufacturers pursue lightweighting strategies and electric vehicle development. Structural bonding applications enable the joining of dissimilar materials in multi-material vehicle designs, while composite applications utilize epoxy matrix systems for body panels, interior components, and structural elements. Battery encapsulation and thermal management applications in electric vehicles require specialized epoxy formulations with exceptional thermal properties and long-term reliability.

Electronics and electrical applications represent a high-value market segment where epoxy resins serve critical functions in component protection, circuit board manufacturing, and electrical insulation. Semiconductor encapsulation utilizes ultra-pure epoxy compounds to protect sensitive electronic components from environmental damage while maintaining electrical performance. Printed circuit board applications rely on epoxy-based laminates and prepregs for structural integrity and electrical insulation.

Other Trending Reports

https://www.databridgemarketresearch.com/reports/global-grape-seed-flour-market

https://www.databridgemarketresearch.com/reports/global-next-generation-solar-cell-market

https://www.databridgemarketresearch.com/reports/global-fish-protein-hydrolysate-market

https://www.databridgemarketresearch.com/reports/global-hydrolyzed-collagen-market

https://www.databridgemarketresearch.com/reports/global-memory-foam-mattress-market

https://www.databridgemarketresearch.com/reports/global-organic-fruits-and-vegetables-market

https://www.databridgemarketresearch.com/reports/global-smart-aquaculture-market

https://www.databridgemarketresearch.com/reports/global-impetigo-therapeutic-market