AML and Fraud Detection Strategies Transforming In-House Mortgage Lending in 2026

These tools improve detection accuracy while reducing manual review times and operational bottlenecks. Researchers have highlighted the growing effectiveness of graph-based analytics and adaptive learning systems in uncovering hidden relationships between fraudulent entities, mule accounts, and synthetic identities.

AML and Fraud Detection Strategies Transforming In-House Mortgage Lending in 2026

The mortgage lending landscape in 2026 is evolving rapidly as financial institutions face rising pressure from sophisticated cybercrime, synthetic identities, deepfake documentation, and increasingly complex regulatory expectations. As digital lending ecosystems expand, mortgage providers are redesigning risk management frameworks to protect borrowers, maintain compliance, and preserve operational trust. One of the most important developments shaping this transformation is the convergence of compliance monitoring with intelligent risk analytics.

The growing use of AI-generated financial documents and identity manipulation has forced lenders to strengthen verification systems across the entire loan lifecycle. Industry analysts report that fraud attempts involving automated identity fabrication and manipulated borrower records have increased significantly over the past year, particularly in high-volume mortgage origination environments.

Real-Time Risk Intelligence Is Becoming Essential

Traditional rule-based monitoring systems are no longer sufficient for modern mortgage operations. In 2026, lenders are increasingly adopting real-time analytics platforms capable of detecting suspicious borrower behavior within seconds. These systems evaluate transaction histories, employment inconsistencies, property valuation anomalies, device fingerprints, and behavioral signals simultaneously.

The shift toward instant risk assessment is being driven by the rise of digital-first mortgage applications and faster approval expectations. Advanced analytics models can now identify abnormal lending patterns before a loan is finalized, reducing exposure to organized fraud networks and money laundering schemes. Financial crime experts emphasize that institutions must move from reactive investigations toward predictive risk management strategies.

This evolution is particularly important for internal mortgage lending operations, where streamlined approval workflows can unintentionally create vulnerabilities. Modern risk engines now combine credit scoring, customer due diligence, and suspicious activity monitoring into unified decision-making systems.

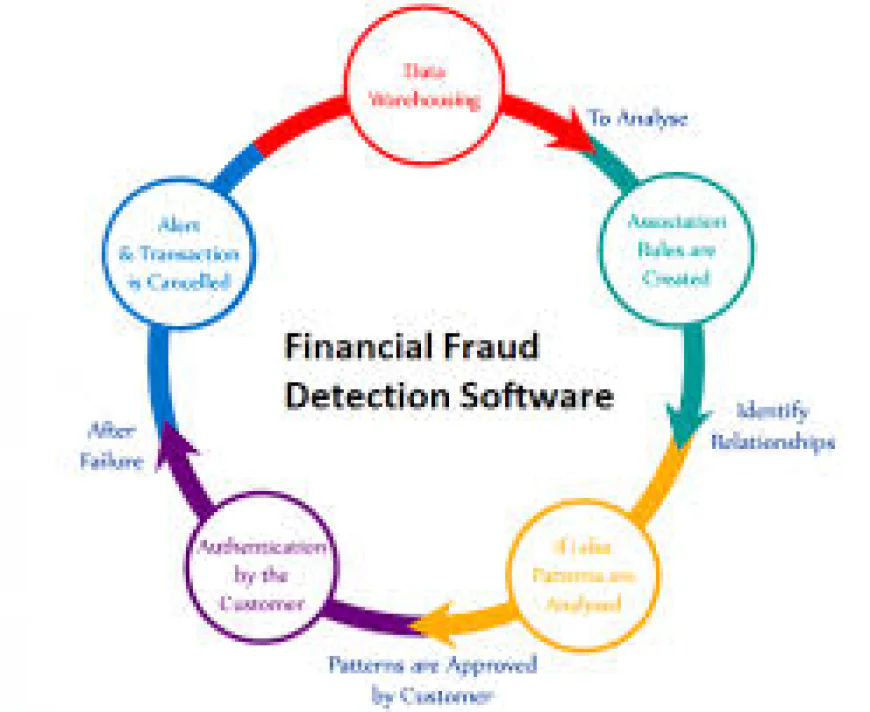

Artificial Intelligence Is Reshaping Fraud Prevention

Artificial intelligence has become central to detecting hidden fraud indicators in mortgage applications. Machine learning models can analyze thousands of data variables at scale, identifying subtle inconsistencies that human reviewers may overlook. These tools improve detection accuracy while reducing manual review times and operational bottlenecks.

Researchers have highlighted the growing effectiveness of graph-based analytics and adaptive learning systems in uncovering hidden relationships between fraudulent entities, mule accounts, and synthetic identities. These technologies help lenders identify coordinated fraud attempts across multiple applications and financial channels.

At the same time, lenders are implementing continuous monitoring frameworks that evolve alongside changing criminal tactics. Instead of relying solely on historical fraud patterns, adaptive systems can learn from new attack methods and update risk indicators dynamically. This capability is becoming critical as financial criminals increasingly use generative AI tools to create convincing fake identities and financial records.

The integration of intelligent automation into mortgage compliance workflows is also improving operational efficiency. Automated case management, document verification, and transaction screening reduce processing delays while enabling compliance teams to focus on higher-risk investigations.

Unified Compliance Models Are Redefining Mortgage Security

Another major trend in 2026 is the convergence of compliance, fraud prevention, and customer risk management into a single operational framework. Industry experts note that separating fraud monitoring from anti-money laundering programs creates visibility gaps that sophisticated criminals can exploit.

As a result, lenders are increasingly adopting integrated financial crime platforms that combine customer identity verification, sanctions screening, transaction analysis, and behavioral monitoring into one ecosystem. This connected approach improves investigative accuracy and helps institutions detect broader criminal networks rather than isolated suspicious activities.

The use of centralized data environments also enables lenders to build stronger borrower risk profiles. By connecting customer interactions across digital channels, institutions gain a more complete understanding of borrower behavior and transaction legitimacy.

The growing importance of aml and fraud detection within mortgage lending operations reflects a broader industry shift toward proactive security, intelligent automation, and real-time compliance management. As financial crime techniques become more advanced, mortgage providers that invest in adaptive analytics, AI-powered verification systems, and unified risk intelligence will be better positioned to protect both institutional assets and borrower trust in the years ahead.